Oil and Gas Firms Are Saddling States with Billions in Cleanup Costs, “It’s like a game of hot potato.” by Nick Bowlin  The problem is much worse in Alberta, thanks to law violating, no duty of care, corporate crime enabler, AER.

The problem is much worse in Alberta, thanks to law violating, no duty of care, corporate crime enabler, AER.

This story was originally published by High Country News and is reproduced here as part of the Climate Desk collaboration.

When an oil or gas well reaches the end of its lifespan, it must be plugged. If it isn’t, the well might leak toxic chemicals into groundwater and spew methane, carbon dioxide, and other pollutants into the atmosphere for years on end.

But plugging a well is no simple task: Cement must be pumped down into it to block the opening, and the tubes connecting it to tanks or pipelines must be removed, along with all the other onsite equipment. Then the top of the well has to be chopped off near the surface and plugged again, and the area around the rig must be cleaned up.

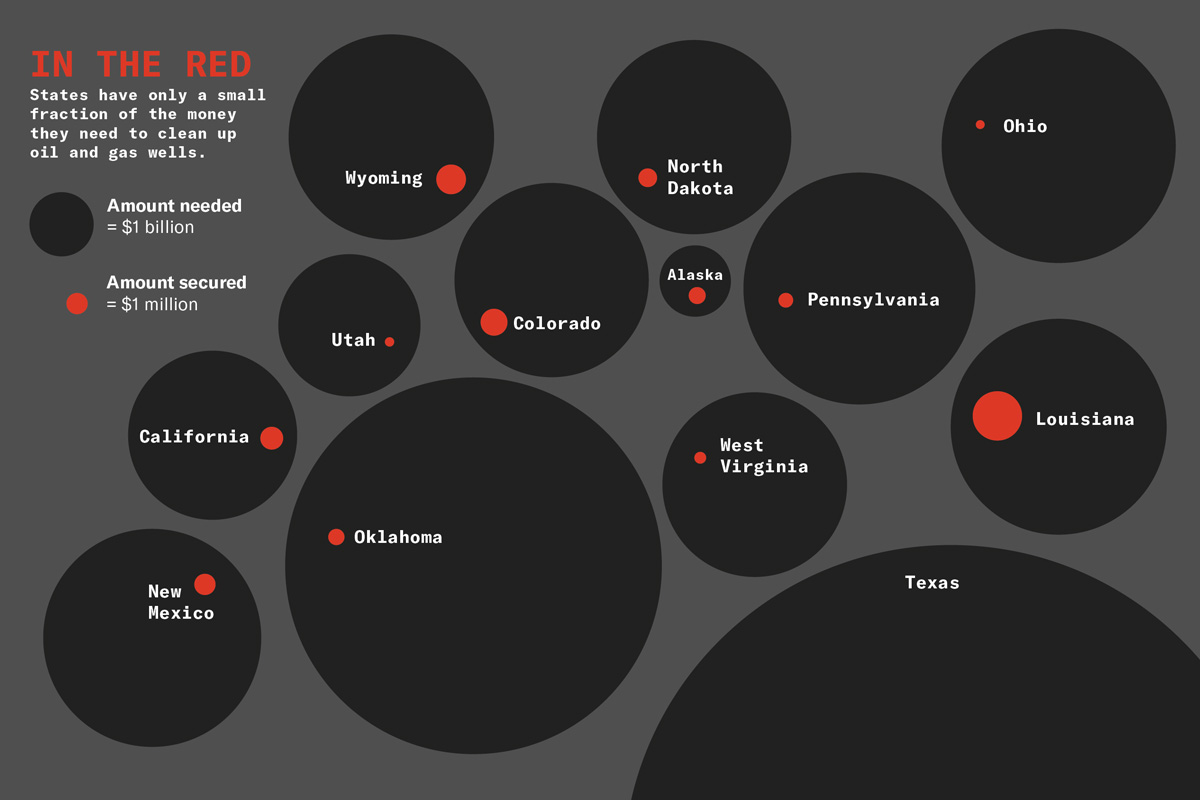

There are nearly 60,000 unplugged wells in Colorado in need of this treatment—each costing $140,000 on average, according to the Carbon Tracker, a climate think tank, in a new report that analyzes oil and gas permitting data. Plugging this many wells will cost a lot —more than $8 billion, the report found.

Companies that drill wells in Colorado are legally required to pay for plugging them. They do so in the form of bonds, which the state can call on to pay for the plugging. But as it stands today, Colorado has only about $185 million from industry—just 2 percent of the estimated cleanup bill, according to the new study. The Colorado Oil and Gas Conservation Commission (COGCC) assumes an average cost of $82,500 per well—lower than the Carbon Tracker’s figure, which factors in issues like well depth. But even using the state’s more conservative number, the overall cleanup would cost nearly $5 billion, of which the money currently available from energy companies would cover less than 5 percent.

This situation is the product of more than 150 years of energy extraction. Now, with the oil and gas industry looking less robust every year and reeling in the wake of the pandemic, the state of Colorado and its people could be on the hook for billions in cleanup costs. Meanwhile, unplugged wells persist as environmental hazards. This spring, Colorado will try to tackle the problem; state energy regulators have been tasked with reforming the policies governing well cleanup and financial commitments from industry.

“The system has put the state at risk, and it needs to change,” said Josh Joswick, an organizer with the environmental group Earthworks. “Now we have a government that wants to do something about it.”

… The oil and gas industry is already mired in a years-long decline that raises doubts about its ability to meet cleanup costs. In six out of the past seven years, energy has been either the worst- or second-worst-performing sector on the S&P 500. …

The deep divide between the true cost of cleanup and what industry has so far ponied up is not news to Colorado regulators. In a 2017 letter to lawmakers, the COGCC estimated that the average costs of plugging wells and cleaning up the drilling site “exceed available financial assurance by a factor of fourteen.” …

But as it stands today, oil and gas companies aren’t realistically paying anywhere near the true cost of cleaning up their drilling sites. And with the industry’s murky financial future, experts predict more and more sales of risky wells to less-wealthy operators, until the state could end stuck with the final cost.

“It’s like a game of hot potato,” Williams-Derry said, “except that when the potato goes off, it’s the public who loses.”

U.S. shale prioritizing debt over drilling, just as OPEC predicted by Michael Tobin, David Wethe and Kevin Crowley, March 12, 2021, World Oil

Saudi Arabia’s bet that the golden age of U.S. shale is over appears to be a safe one — for now, at least.

A round-up of data on shale drillers shows they’re sticking to their pledge to cut costs, return money to shareholders and reduce debt. If they stay the course, it would validate the OPEC+ alliance’s high-stakes wager that it can curb output and drive crude prices higher without unleashing an onslaught of supply from U.S. rivals.

That’s still a big “if,” one that’s keeping the oil market on edge as crude’s rally makes it more tempting for shale producers to go back on their word. But the U.S. shale patch is showing little sign of a true comeback so far, and even a dramatic boost in activity would leave oil output below pre-pandemic levels until late next year. Drillers that have shown signs of straying from the script and boosting production have been punished by investors.

Publicly traded explorers that are remaining disciplined on output are helping to keep crude prices aloft, said Michael Tran, managing director for global energy strategy research at RBC Capital Markets. The motives of closely held producers, on the other hand, remain “an open-ended question,” he said. The number of oil rigs has already jumped 80% after bottoming out in August, Baker Hughes data show.

The more restrained shale drillers are this year, “the more they can potentially grow production at higher prices next year and beyond,” Tran said.

As crude prices climb, the odds of another shale boom rise, JPMorgan Chase & Co. analysts including Natasha Kaneva wrote in a March 11 note to clients. Even with flat capital spending, efforts are under way to maintain or grow production at low cost, according to the bank.

“At current prices, most U.S. onshore operators are economic, leaving a vast group of operators, from large public companies to private players, in good position to ramp up activity” in the second half of this year and build solid momentum for higher output in 2022, the analysts said.

Bloomberg compiled these charts from Bloomberg Intelligence data of publicly listed companies. Companies with production outside of the U.S. are excluded.

Muted Output

Producers are keeping their powder dry and barely increasing production at a time when oil prices are recovering to pre-pandemic levels. Companies are instead focused on reducing debt and paying cash back to shareholders through dividends.

Companies that recently announced plans to boost output, like Matador Resources Co. and EOG Resources Inc., saw a drop in their share prices.

Tight Reins

Capital discipline is the name of the game now. Exploration and production companies are focused on generating free cash flow and strengthening their balance sheets. “What we really need to do is maintain our scale and generate free cash, excess substantial free cash, and push that into reducing debt,” Ovintiv Inc. [previously Encana] Chief Executive Officer Doug Suttles said in an interview with Bloomberg Television.

Efficient Drilling

Even as producers cut capital spending, they can keep output flat or slightly higher compared with last year. That’s because as oilfield service companies continue to get better at drilling and fracking, the explorers who hire them are getting more bang for their buck.

For an explorer to turn a profit in the Permian’s Delaware, the lowest-cost U.S. basin, an oil price of roughly $33 a barrel is required, down from $40 in 2019, according to BloombergNEF. So-called break-evens refer to the price at which the cost of bringing supplies online is less than or equal to the expected revenue. West Texas Intermediate crude settled at about $66 a barrel on Thursday.

“Contract renegotiations, ongoing efficiency gains and process improvements have allowed the oil industry to slash the cost to drill and complete a well,” according to the report.

Production Lags

This year’s surge in oil prices should mean the number of rigs will continue to climb from its historic lows, particularly as closely held operators take advantage of higher revenues.

But even if drilling expands at a much more aggressive pace than companies are promising, it will be a long time before U.S. shale production reaches its peak again, according to a projection by ShaleProfile Analytics. If the rig count doubled by the end of the year and then holds flat, it would take until the end of 2022 before the industry regains the production it lost during the pandemic, the projection shows.

The model assumes no changes in well productivity or in the number of drilled but uncompleted wells.

Merger Wave

A year of consolidation in the shale industry put a lid on production. Companies including Concho Resources Inc. and Parsley Energy Inc., which once drilled aggressively, have been acquired by larger rivals. Producers are turning their attention inward and focusing on returning capital to shareholders rather than getting more oil out of the ground.