Shell Exits The Marcellus Shale, Losing $4.1 Billion And Raising Questions by Josh Young, May 5, 2020, Seeking Alpha

Shell is selling their Pennsylvania Marcellus asset for $541 million.

They bought it for $4.7 billion dollars.

Divestiture seems poorly timed considering North American natural gas fundamentals versus the rest of Shell’s business.

Royal Dutch Shell (RDS.A) is selling their Pennsylvania Marcellus Shale asset to National Fuel Gas (NFG) for $541 million. This compares poorly to the price they paid to buy the asset from KKR (KKR) backed East Resources in 2010: $4.7 billion. Losing more than $4.1 billion on an asset round-trip, before factoring in capital spent on developing the asset, raises some additional questions about Shell’s management and business model beyond those addressed in “Covid-19 Breaks The Super Major Business Model“.

First the transaction. In the acquisition of the asset, it was disclosed that current production was 60 mmcf/d, and that it included “650,000 net acres of ‘highly contiguous, operated acreage’ in the region and 1.05 million net acres in the Marcellus Shale overall.” In the divestiture of the asset, current net production is disclosed as 250 mmcf/d and net acreage is 450,000 acres. Likely substantial capital was spent developing the asset to increase production 4x, while a large portion of the lease position was allowed to lapse, with the acreage position declining from 1.05 million net acres to 450,000 net acres.

This raises a few questions and concerns beyond Shell’s recent dividend cut, share price fall, and the oil and LNG price crashes that precipitated it. These include: 1) what was the vision for the asset and the company at the time of the $4.7 billion purchase? 2) what changed about the asset and/or company plan such that this same asset was sold for $500 million 10 years later? and 3) are there bigger problems at Shell that pushed it into a dividend cut at a time when peers maintained their dividends?

1) In reviewing Shell’s annual report from 2010, the year it bought the Marcellus asset for $4.7 billion, and the “strategy” corporate presentation from 2011, the vision and some flaws become apparent. In the annual report, the Marcellus acquisition is classified as an opportunity for “growth beyond 2012” – years into the future. And in the strategy presentation, Shell shared its effective natural gas price forecast, targeting a total “breakeven price” including entry cost of over $4/mcf and an “expected gas price range” of $4-8/mcf. …

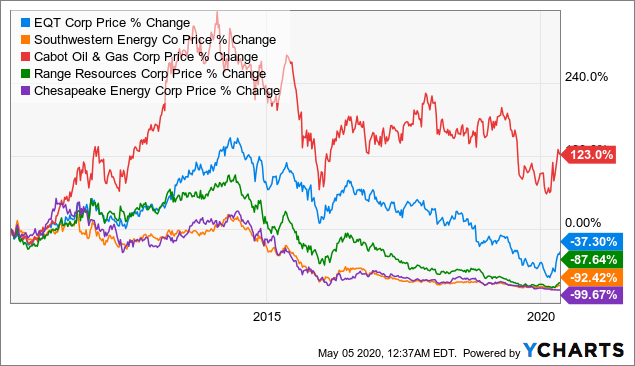

2) … Shell was clearly unable to sufficiently reduce its gas production costs and improve its production efficiencies sufficiently to effectively compete. One could argue that this was not a promising competition to engage in, as the longer term share price performance of these natural gas producer competitors, excluding Cabot, has been abysmal:

This is indicative of a challenge to extract economics in what has been a natural gas producer “race to the bottom,” which has crushed the shares of gas producers besides Cabot and has, among other problems, likely bankrupted Chesapeake (CHK).

3) Like Shell, Chevron (CVX) recently took a multi-billion dollar loss on its Marcellus assets. This indicates a broader challenge in applying the integrated super major business model to the upstream unconventional natural gas business. One possibility is oil major difficulty in extracting costs and improving well productivity as effectively as smaller and more nimble companies. Another is that the majors size may have limited their asset purchase selectivity, leading to too high a price paid for too low quality assets.

I identified this problem previously in the context of the majors’ activity in the Duvernay shale, a play somewhat similar to the Marcellus. Shell, Chevron and others overpaid for moderate quality Duvernay land and then struggled with cost efficiencies and well productivity.

And like in the Marcellus, Shell bought Duvernay Oil for $5.9 billion in 2008 and after struggling with the assets, resold the bulk of them for $1 billion to Tourmaline Oil (OTCPK:TRMLF) in 2016.

There are other implications of Shell’s $4.1 billion loss in the Marcellus. The asset sale is timed close to the announcement of Shell’s first dividend cut in 70 years. This could either be a “kitchen sink” moment, where Shell is trying to get as much bad news out as possible at once. Or it could be indicative of deeper asset or liquidity problems. For such a big company, it is hard to imagine a $541 million asset sale would move the needle, particularly considering recent debt issuance. But it could indicate a new unwillingness to tolerate under-performing or money losing assets.

One final consideration: after years of under-performance, natural gas prices have started to recover as shale oil activity is falling and is bringing associated gas production down along with it. Natural gas focused producers are seeing their share prices outperform, in some cases substantially. This is a curious environment in which to sell a natural gas asset at an almost 90% loss, indicating some degree of inertia or liquidity need. ![]() Or, Shell realized it was not creative enough to keep investors sinking their money into the frac con.

Or, Shell realized it was not creative enough to keep investors sinking their money into the frac con.![]()

Refer also to:

2012: A fracking disgrace: Shell’s monitoring team